This Investor Doesn't Need Your Exit

Peter Langmar, CIO at STRT, on backing profitable founders

👋 Hi, it’s Zdenko, welcome to 185 new readers since the last edition.

Seedstrapped is a newsletter for founders building profitably growing businesses without riding the VC treadmill (and for investors who get it).

If you’re new here, start with some of the most-read issues:

I received this message from Roland Kovacs, an Investment Manager at STRT Holding (STRT) on Linkedin:

I liked your post because it shows how the traditional VC playbook is broken and the focus is shifting towards profitability in todays economy, especially in the CEE region. At STRT we believe in the same, thats why we operate differently from traditional VC.

I immediately wanted to learn more. This is not something you hear often from investors.

Roland connected me with Peter Langmar, the Chief Investment Officer at STRT, who agreed to share some of their learnings with me and other founders.

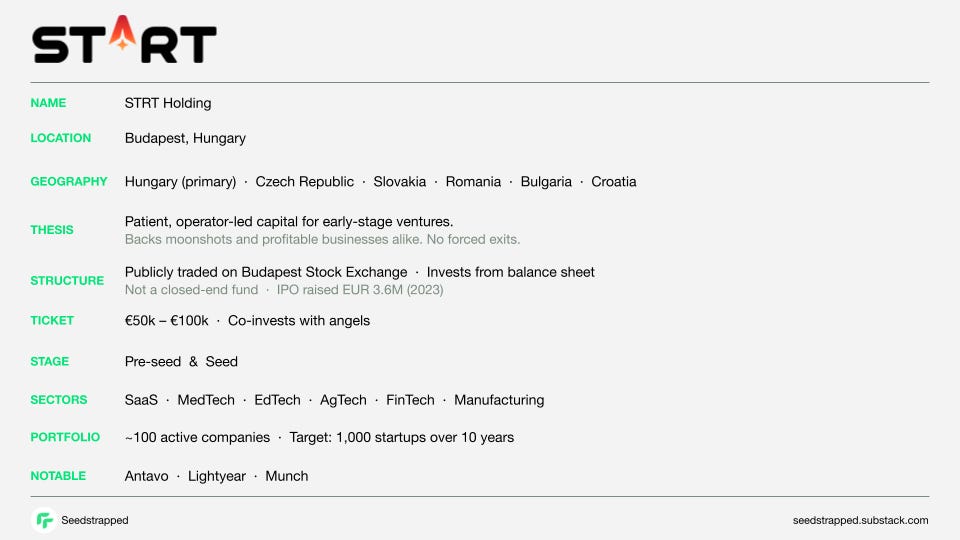

STRT is a publicly traded investment vehicle based in Budapest with roughly 100 active portfolio companies and an ambition to back 1,000 startups over 10 years.

Before joining STRT, Peter co-founded an IT education bootcamp that expanded across Central Europe and sold it to a private equity firm in 2022.

STRT is unusual in another way too: alongside investing, it runs a profitable education business that trained over 3,100 people in 2024 - portfolio companies get access at cost.

Here are 5 things that stood out from our conversation.

1. The fund structure is the strategy

Most founders focus on the investor’s thesis. Peter thinks you should focus on their structure first.

Classic VC funds are closed-end vehicles. They raise once, deploy over a few years, and must return capital within a fixed window. That creates pressure to exit whether the timing is right or not. A VC fund simply cannot stay in a profitable, slow-growing company that pays dividends - the maths do not work for them.

STRT invests from its own balance sheet as a publicly traded company. There is no fund lifecycle forcing a sale. As Peter put it:

We don’t force exits. We don’t ask for drag rights. We are patient.

For seedstrapped founders, that distinction is everything.

2. Seedstrapping is not new. It just finally has a name.

When I asked whether seedstrapping is a lasting model or a buzzword born from the post-2022 capital drought, Peter was grounding:

This is how all successful SMEs have been built. Someone put in initial capital and the business grew from there. There is nothing new about it.

What is new is how we talk about it in the startup context. A decade of VC-as-default thinking created a generation of founders who assume raising every one to two years is normal - even when their business does not need it.

The companies that quietly built real cash flow and sold for eight-figure sums were always there. We just were not writing newsletters about them.

3. Know what kind of business you are actually building

STRT’s portfolio spans surgical hardware, manufacturing, SaaS, student discount platforms and more. Peter does not believe in one-size-fits-all funding advice.

A deep-tech medical device needs a decade and hundreds of millions before it earns a euro. That is not a seedstrapping story. But a manufacturing company making tiny houses in Romania? They raised from STRT and a few angels, stopped there, and have been growing organically ever since.

One of their student discount platform investments made the same pivot - originally pitched the moonshot, then realised their cash flow was stronger than their growth ceiling and expanded to a neighbouring country without raising another round.

Peter’s rule of thumb: if you need massive capital just to reach the starting line, venture is probably the right tool. If you can reach customers and generate cash within a year or two, there is a real question about whether you should raise at all.

4. Liquidation preference is where founders lose money they never knew they had

Peter is unusually direct about something most investors gloss over.

“You need to do the math,” he said. “What does it take to raise X amount and still have something meaningful at exit?” A company can reach an impressive paper valuation, but after multiple rounds and liquidation preferences, a founder may walk away with less than someone who raised once, stayed lean, and sold a smaller business five years earlier.

The math is not always obvious. But it is always there.

5. Three things Peter would tell every founder

When I asked for his one big lesson, he gave me three.

1/ understand what kind of life you are signing up for. Whichever path you choose, you are committing at least a decade. The paths look very different ten years in — know which one you actually want before you start.

2/ understand your investor’s business model. What do they need from you? An investor who must close a fund in year eight will behave very differently from one who can hold indefinitely.

3/ run the liquidation preference scenarios before you sign anything. Most founders do not. It is one of the most expensive oversights in early-stage funding.

My reflection

What makes STRT interesting is not just the thesis - it is the honesty about structure. For founders who want to raise once and grow on their own terms, the question is not only whether a VC “gets it”, but whether their structure even allows them to support that path long-term. Most closed-end funds cannot. STRT can. That is worth knowing.

Four things in particular stand out to me about how they are set up.

First, the education arm. STRT runs a profitable training business that funds a significant part of their operations. That means they are not dependent on management fees from a fund - the lights stay on regardless of how the portfolio performs in the short term. That changes the incentives in ways that matter for founders.

Second, the public company structure. Being listed on the Budapest Stock Exchange is unusual for an early-stage investor, but it has real advantages. It gives their investors daily liquidity - anyone can buy or sell a single share for a few euros - which lowers the barrier to entry dramatically compared to a traditional fund with a €200k minimum. It also means STRT is accountable to public markets, which creates a different kind of discipline than a private fund where reporting is limited to LPs.

Third, it is run by people who have actually built and sold companies. Peter sold an IT bootcamp to private equity. STRT founder Péter Balogh built and exited one of Hungary’s most successful software businesses. That is not common in the region, where many early-stage funds are run by people who have spent their careers on the investment side. The difference shows up in how they engage with founders - less theory, more pattern recognition from lived experience.

Fourth, they are genuinely flexible on investment model. STRT holds surgical hardware startups alongside profitable manufacturing businesses and dividend-paying platforms. They are not forcing every company into the same VC growth template. That flexibility is rare, and for founders who do not fit the standard mould, it matters.

To get in touch with Peter and his team, write to invest@strt.hu or visit their website. A warm intro always helps, but cold emails are read.

PS: We’re investing $100k–$500k in 1-2 seedstrapped businesses this quarter with Flying Founders. If you’re raising once and building for profitability, let’s talk.